As consumer goods have been shrinking in size, prices have been climbing at a record pace. Central banks have been raising interest rates to push down inflation as recession worries continue to loom. So, whose hands are in your pockets these days anyway? The normal culprits such as gas and food keep fuelling the weekly headlines. Gas continues to fluctualize, finding a fluctuating range in a realm of stability that has eased price ceiling shock, yet still impacts the bottom line. Meanwhile, food has soared to its highest level in decades, spawning a watchdog investigation into the grocery industry. Both fuel and food continue to eat up consumer budgets and spending habits, impacting mortgages and other spending behaviours.

FIVE DOLLARS PLEASE

Gone are the days when I’d hear my mom say, “Five dollars please,” at a full-service gas station and that would get us 25 litres of fuel and the windshield washed. Today, five dollars would fetch about 3 litres of fuel, a sliver from having to wash my own windshield, and someone in the next car honking at me to hurry up. Of course, it’s unreasonable to expect 1979 fuel costs, but a little consistency could go a long way in budget planning.

There was a period of relative stability between 1981 and 1999 where prices sat between 40-60 cents per litre. Then the next decade would see a steady climb reaching just over $1.20 around 2008. Since then, it’s been a roller coaster as the price has dipped below $1 and climbed almost as high as $2 per litre. Each increase and decrease sending people in waves to fill-up to save a few dollars.

Today’s average gas tank is about 55 litres, so at $1.62/litre filling up from empty costs about $89.10. By comparison, five years ago the cost sat around $1.29/litre and a 55-litre tank would cost you $70.95. That’s almost a $20 increase per tank which amounts to about $1,100 more per year on a weekly fill.

FOOD TRANSPORTATION COSTS

If it costs more for you to get around, it also means that it costs more for food to get to you and that has arguably been one of the factors impacting the record food costs. While manufacturers have compensated by reducing the size of some products to curb increases, not everyone is buying into “shrinkflation”, although we are left to wonder as I previously wrote in late spring, “Is Shrinkflation Here to Stay?”

Product size aside, the costs have been increasing year over year with some exceptions in 2020. Looking at 38 common products shows a consistent rise is produce, meat, condiments, dairy, vegetables, fruit, and more. Some may say, "well meat is only 75 cents more per kilogram, and apples are only 30 cents more per kilogram, and butter is only 40 cents more", but each of these add up to a bigger bill and maybe smaller dishes at the kitchen table as families apply their own version of shrinkflation.

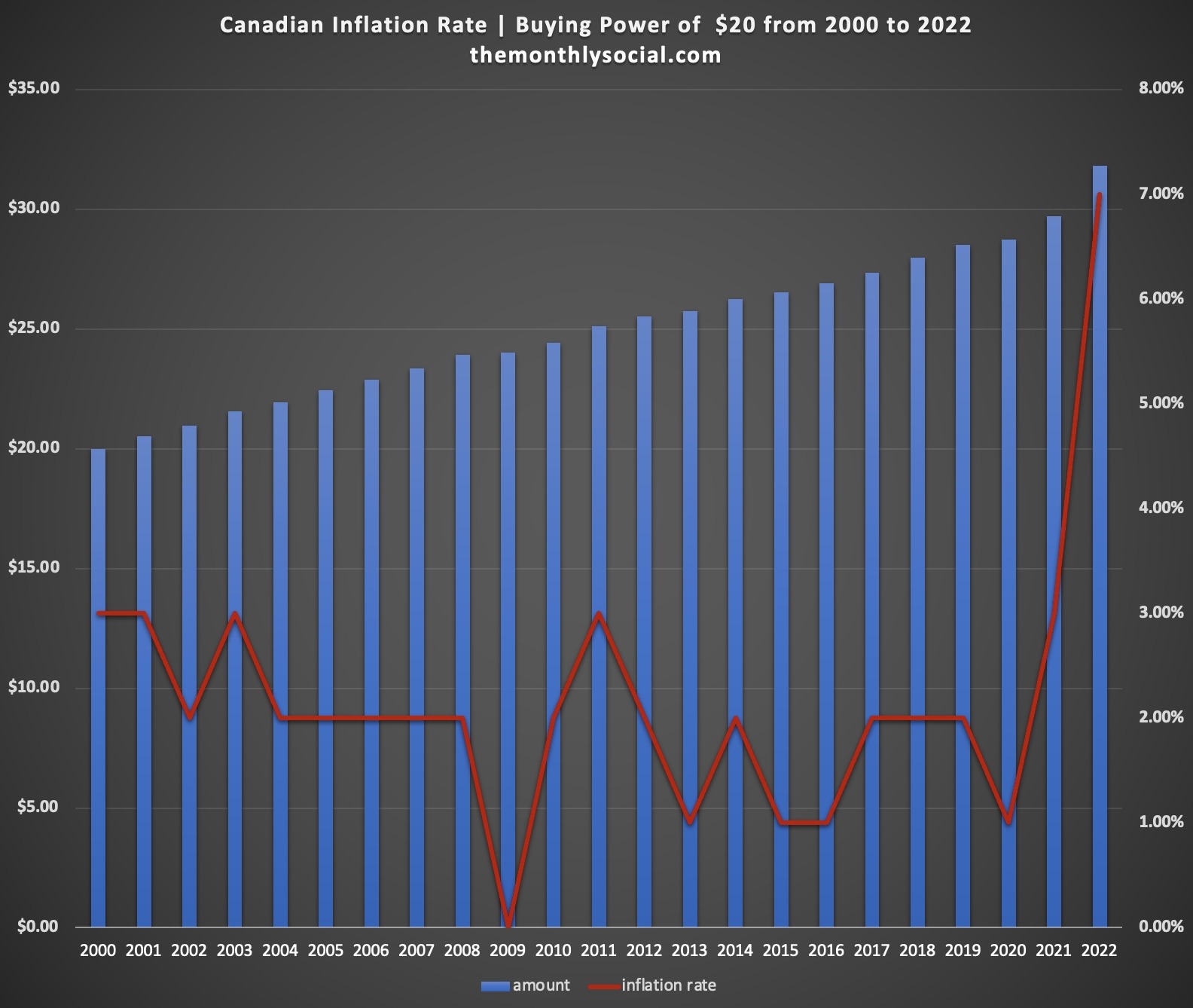

BUYING POWER

With food packages shrinking and the value of the dollar falling, you must spend $23.28 in 2022 to get the same amount of food product that $20 bought in you in the year 2017. When you look at it over the past 22 years, that same $20 would cost you $31.83 by comparison. What is more alarming than the buying power of the dollar is the escalated rate of inflation in 2022 as it sits at 7% and isn’t showing any signs of slowing down, despite the central banks cranking up interest rates. It’s an alarming trend that is fuelling recession speculation, especially when you consider the inflation rate in 2021 was at 3%, in 2020 it was 1%, and for the three years prior it held steady at 2%.

THE FOOD WATCHDOG

As grocery chains set record gross profit margins, consumers show little sympathy for their argument that they’re faced with record operating costs, some even accusing them of profiteering. In late October, Canada’s Competition Bureau said that it will investigate the grocery industry, forwarding improvement recommendations to the government. This on the heels of Loblaws announcing that they would “freeze” no-name product prices to the end of January 2023 to help consumers cope with grocery increases. The news is somewhat welcome, although not everyone is rushing to Loblaws with open arms as consumers point out that the freeze doesn’t reduce any of the recent price increases and that Loblaws stands to make greater profits on its self-branded products. Shortly after the announcement, Metro, another grocery chain called out Loblaws, potentially exposing it as a public relations stunt because most grocery stores usually freeze prices heading into the holiday season.

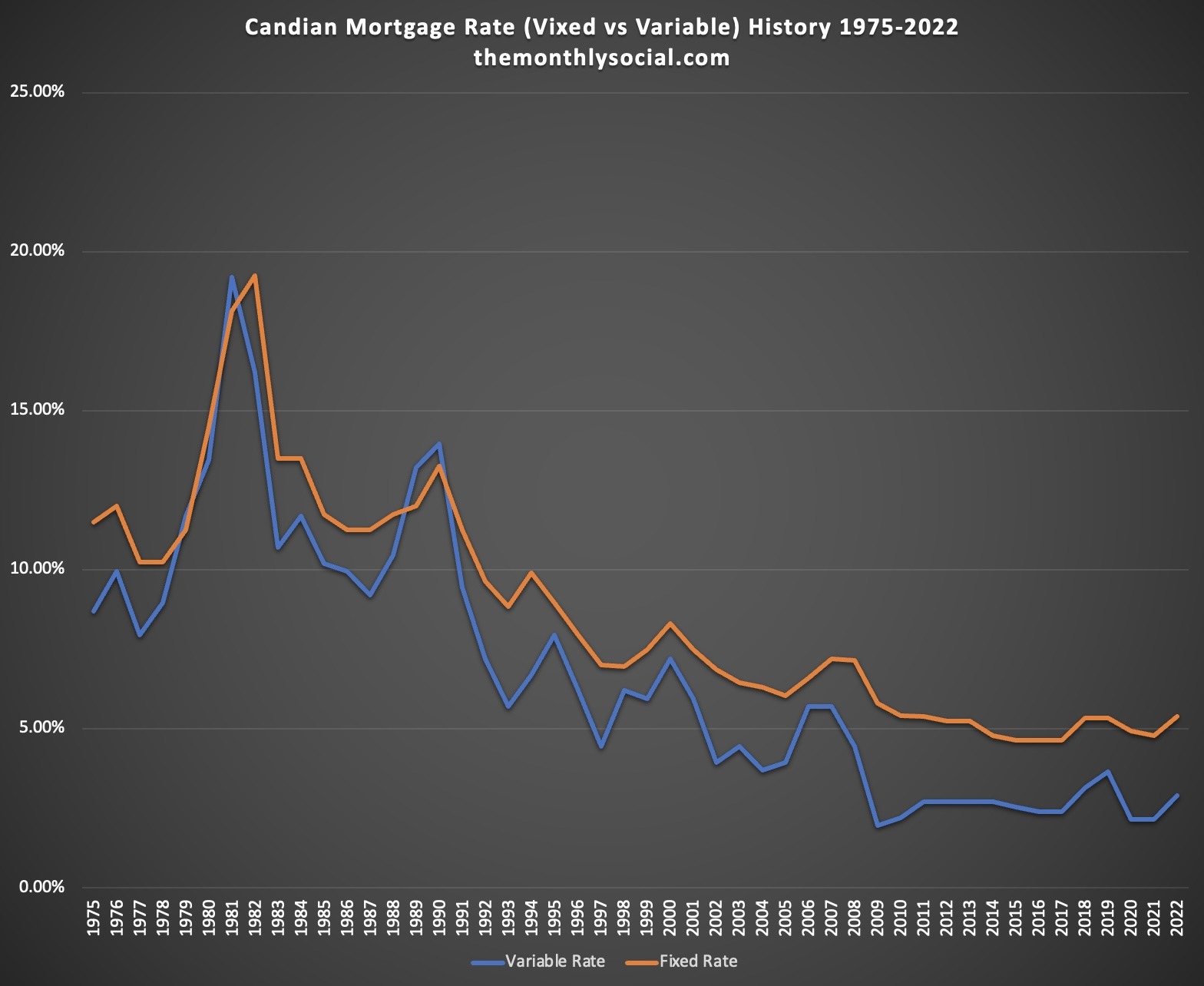

RISING MORTGAGE RATES

With increases in fuel and food, consider yourself lucky if you signed a new mortgage or renewed your mortgage before the climb in interest rates. As the central banks increase the prime rate as a tool to curb inflation, it has driven the mortgage rates soaring above 5% for a fixed rate, with variable rates following behind at 3%, both numbers that haven’t been consistently seen since 2008.

The amount paid in principal and interest can make a significant difference in how far your money will go. For example, if you take a mortgage of $300,000 amortized over a period of 25 years for a term of 5 years and compare the difference between 3% and 5% interest, you’ll be putting less money down on the principal amount, pay more money in interest, and come out in five years north of $260,000 still owed. The only way to reach a comparable outcome to the 3% interest rate is to decrease your amortization to 20 years, but that will drive up your monthly payments taking money out of your current budget flow that you may need elsewhere to survive.

This example used a fixed rate of 5%, but as was discussed on The Monthly Social Podcast with long-time Mortgage Broker Ron Butler, variable mortgages have typically performed better over the last 40 plus years except for the early 1980’s and 1990’s and that has always been the risk associated with a variable over fixed mortgages.

HOME FARMING

As people grapple with increases in fuel, food, and mortgages, they are also looking for alternative ways to feed their family while remaining health conscience and stretching their dollar. Warm climate months afford an opportunity where gardens can produce summer helpings and fall preserves, but as winter approaches that source of food is eliminated. Green thumbs like The Monthly Social Podcast November guest, Patty Greve, have found a way to garden in-door all year round using a modern aeroponic system.

Aeroponics and Hydroponics are an alternate growing solution that was covered in January on The Monthly Social Podcast where the future of farming and potential food costs was explored, before it became more of a reality. Patty provides information on how she does it and how you can do it too, while giving you estimated savings and operating costs that will make you seriously consider her garden tower option.

PLANNING MATTERS

While there is no fail-safe against what may lay ahead with inflation and a possible recession, history and experience tell us that planning, although time consuming can be one of the best tools to use in managing financial impact. That means finding alternatives like aeroponics, hydroponics, maybe clipping coupons, changing spending habits, or even re-thinking vacations and other discretionary spending, albeit some of those changes are exactly what can spawn a recession as consumers hang on to their money longer.

Hopefully there's room left in your pockets for your own hands after everyone has pulled out their share.

This is an opinion article by Guido Piraino of The Monthly Social Podcast. It may also be heard on The Path Radio Mix Online. You can read other opinion articles on the blog page.

For sports content, please consider The Coach's Call YouTube Podcast.